The magic of leverage: buying a 300,000 EUR property using only 60,000 EUR

Imagine you want to buy a property in Marina Alta valued at 300,000 EUR. You have two options:

1. Wait 20 years until you've saved 300,000 EUR (while inflation eats away at your savings and property prices keep rising). 2. Do what the wealthy do: put down 20% (60,000 EUR) and let the bank lend you the rest.

Here's where the first financial miracle happens: you control 100% of an asset using only 20% of your own money. If the property rises 5% in value, you're not earning 5% on your 60,000 EUR — you're earning it on the full 300,000 EUR. Your return multiplies exponentially thanks to the bank's money.

The tenant: your strategic partner

Once you have the property, the game changes. If you've bought well — in a high-demand area like Denia or Jávea — the tenant pays a monthly rent that serves three vital functions:

- Pays the interest and principal on the mortgage. - Covers maintenance costs, insurance, and taxes. - Leaves you with a positive cash flow every month.

In essence: the bank puts up the money, the tenant pays off the debt, and you keep the property. Over time, you own more and more of the home while your debt shrinks and the asset's value grows.

The next level: cash-out refinancing, or the wealth wheel

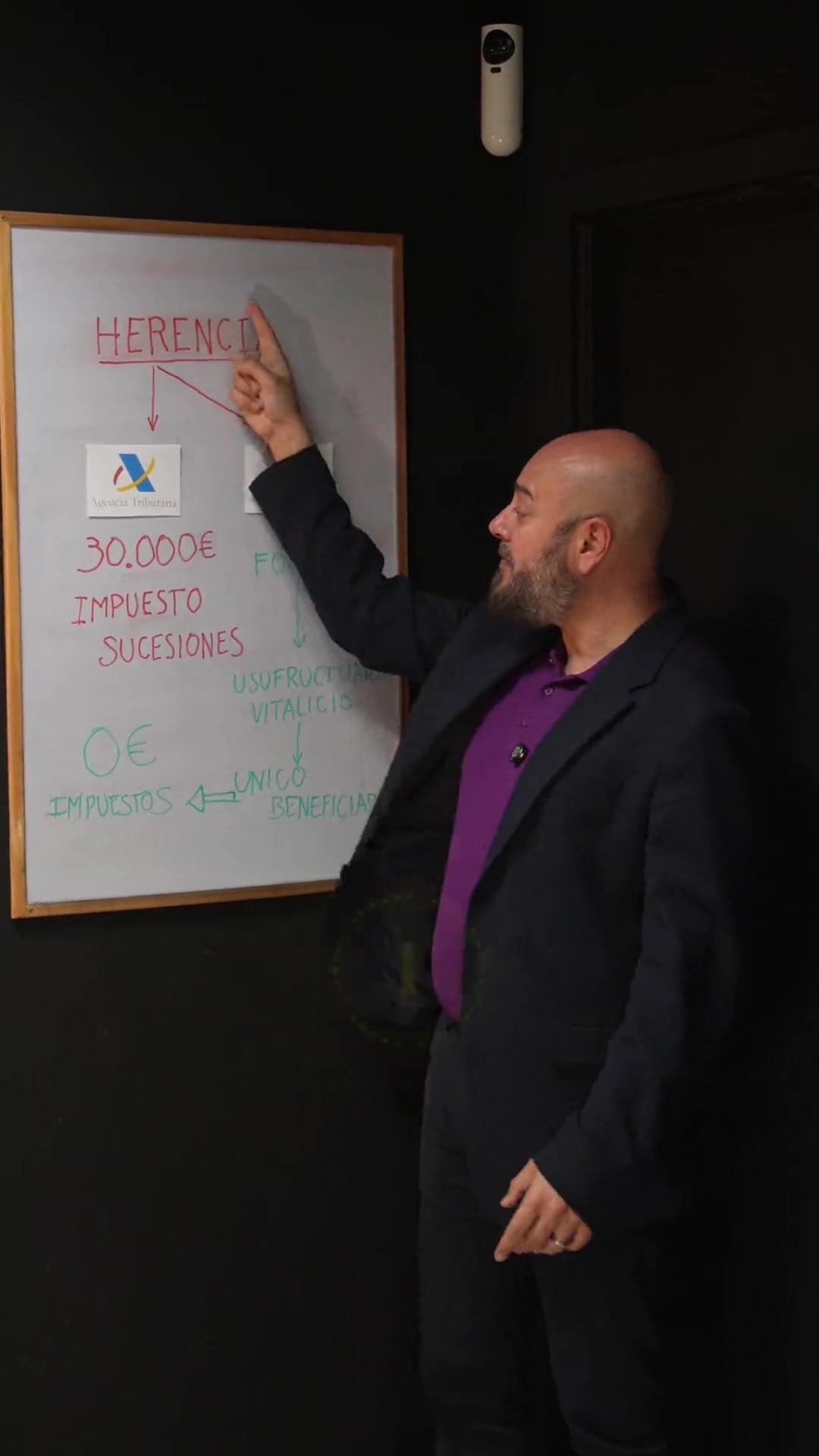

This is where the wealthy become even wealthier. Let's say 8 years pass. Your property in Marina Alta is no longer worth 300,000 EUR — it's now worth 500,000 EUR thanks to the area's appreciation. On top of that, you've already paid off a significant portion of the original mortgage.

Instead of selling the house and paying taxes on the gain, you go to the bank and say: *"My property is now worth half a million. Give me a new loan based on this new value."*

The bank hands you the surplus capital tax-free (because it's a loan, not a sale). With that liquid cash, you make the down payment on a second and third property. What started with a single mortgage has become an entire portfolio. Debt has been the engine of your growth.

Good debt vs. bad debt

In the Reel I mentioned that debt is a springboard, but there's a golden rule that didn't fit in 60 seconds: the net yield vs. interest rate rule.

For debt to be "Good," the net yield generated by renting the property must always exceed the interest rate on your mortgage.

In Marina Alta, due to the strong demand for holiday and medium-term rentals, it's common to achieve yields that comfortably exceed the current financing costs of 2026. If the bank lends you at 3% and your asset yields 6% net, you're earning 3% on money that isn't yours. That's making money out of thin air.

The two types of debt

| Characteristic | Bad debt (passive) | Good debt (active) |

|---|---|---|

| Example | Loan for a car or holiday | Mortgage for a rental apartment |

| Who pays it? | You, with the sweat of your brow | Your tenant |

| Value of the object | Depreciates every day | Appreciates over time |

| Tax impact | None (or negative) | Tax-deductible |

Frequently asked questions

Isn't it risky to have so many mortgages?

The risk isn't the debt — it's vacancy. If you invest in low-demand areas, you take risks. If you invest in Marina Alta, where people always want to live, the risk is minimized because cash flow is virtually guaranteed.

What's the minimum amount I need to start?

Typically you need 20% of the purchase price plus 10-12% for costs (transfer tax, notary, land registry). For a 200,000 EUR property, you'd need approximately 65,000 EUR.

What happens if interest rates rise?

Smart investors in 2026 typically use fixed or mixed rates to protect themselves, or ensure that rental income has enough margin to absorb potential rate increases.